The Address Verification System (AVS) prevents fraud by validating the ownership of a credit card using the billing address of a credit card and matching it with the data on file at the credit card issuing company. You have a wide variety of options available to use AVS for handling transactions that should be declined or approved based on matches of the AVS data.

The AVS checks the numeric portions of the billing address. For example, if you enter 1234 Main Street, Anytown, CA 94107, as the billing address in Chargent, the AVS checks that the 1234 street number matches the 94107 zip code. AVS is supported by Visa, Mastercard, and American Express through most card-issuing banks in the US, Canada, and the UK. Credit cards issued by banks in other countries may not support AVS and should return a response that it is not supported.

AVS Response Options #

The card networks do not decline transactions based on a street address number or zip code mismatch. Instead, they return an AVS response, and you can configure filters in your payment gateway to decline or approve the transaction.

If you are in a business that does not generally experience credit card fraud, you may choose to approve transactions despite mismatches in some or all of the AVS data. For example, some B2B transactions have a low rate of fraud but a higher-than-normal rate of AVS mismatches, as the person using the card could be unaware of the correct billing address on a company card.

Note: Regardless of the AVS response flag, the issuing bank will have authorized the credit card. This means that your customer may have a temporary authorization hold on their card even if your payment gateway settings cause the transaction to be declined.

You may still be able to capture an authorization that received the AVS decline. You should review those orders carefully, and your bank may charge a higher fee on transactions that did not pass AVS checks. Many banks and processors use AVS to avoid non-qualified transaction surcharges. That can add about 1% to transactions, but it may be worthwhile to your business if you have low fraud and a customer from whom you want to take a payment without passing AVS checks.

AVS Configuration #

When configuring your payment gateway filters, review the number of response codes that AVS returns. Choose which ones to reject (decline) and which to accept (approve). Log into the web interface of your payment gateway to configure which codes you want to enforce as filters, rejecting transactions that come back with those AVS codes. Here is a sampling of common codes:

- R = AVS was unavailable at the time the transaction was processed. Retry transaction.

- G = The credit card issuing bank is of non-U.S. origin and does not support AVS.

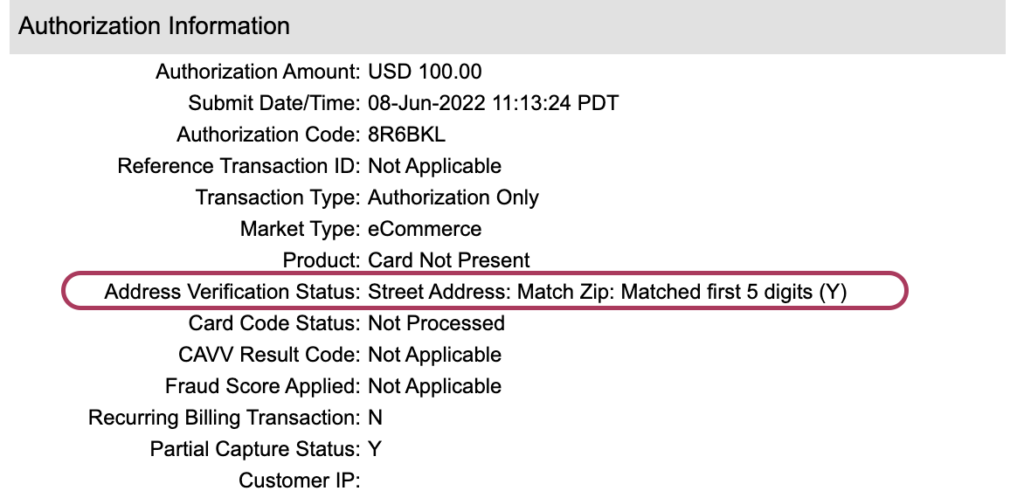

- N = Neither the street address nor the 5-digit ZIP code matches the card’s address and ZIP code on file.

- A = The street address matches, but the 5-digit ZIP code does not.

- Z = The first 5 digits of the ZIP code match, but the street address does not.

- W = The 9-digit ZIP code matches, but the street address does not.

- Y = The street address and the first 5 digits of the ZIP code match.

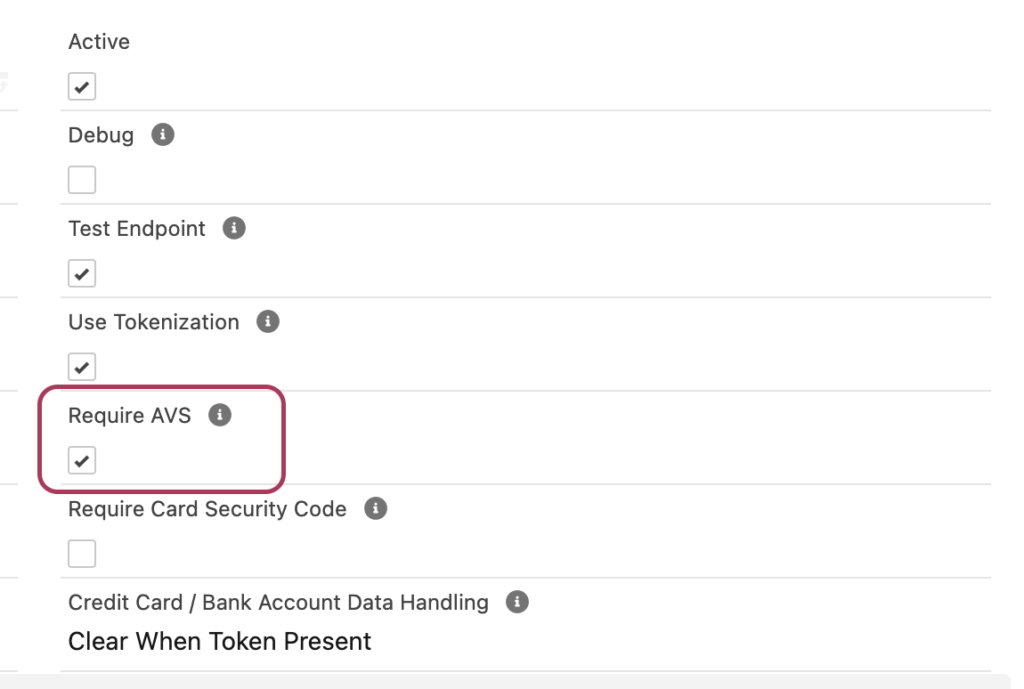

Require AVS Salesforce Field #

The Require AVS field on the gateway record in Salesforce generates an error if it is checked and the Billing Address and Billing Zip/Postal Code fields are blank.

It is always best practice to populate the Billing Address, City, State, and Billing Zip Code/Postcode, as they are often required by the payment gateway. Some gateways, such as Cybersource, also require the Country and Billing Email to be sent.

See Also #

Knowledge Articles

Understanding Chargent Transactions

Chargent Transaction Fields

Chargent Terminology