The Cost of Payment Processing

Payment processing isn’t just a back-office necessity – it’s a cornerstone of doing business. Whether you’re a manufacturer, enterprise, or a subscription-based company, seamless, secure, and efficient payment systems are critical to customer satisfaction and business performance. However, what often gets overlooked is how complex and costly payment processing can be.

This article is designed to educate businesses currently using or evaluating Salesforce for payment processing. We’ll break down the costs involved, uncover hidden inefficiencies, and show how integrating payments directly into Salesforce can lead to significant cost savings, improved efficiency, and a better overall customer experience.

Breakdown of Payment Processing Fees

Payment processing involves multiple fee types, each contributing differently to the overall cost:

Interchange Fees

These are set by card-issuing banks and typically represent the largest share of processing fees. Rates vary by card type, transaction method (in-person vs. online), and the industry sector. For example, B2B manufacturers dealing with high-value invoices might face interchange fees ranging from 2% to 3%, significantly higher than typical retail transactions.

Assessment Fees

Levied by credit card networks (Visa, Mastercard, American Express), these fees are typically a percentage of the transaction and cover the operational costs of maintaining the card networks. Although relatively small per transaction, they quickly accumulate over high transaction volumes.

Processor and Gateway Fees

Payment processors and gateways charge fees for securely transmitting transaction information, conducting fraud checks, and handling the settlement process. These fees can be either fixed per transaction or percentage-based and may vary significantly depending on the chosen provider and additional features used (such as advanced fraud protection or international transaction handling).

These services ensure smooth transaction processing, perform vital security checks, reduce fraud risks, and maintain transactional records. Without these services, businesses would be exposed to significant security and operational risks. Processors invest heavily in cutting-edge security measures, technology infrastructure, and compliance protocols, continuously updating their systems to combat evolving cyber threats and regulatory changes. This ongoing investment ensures secure, reliable, and efficient payment handling.

Merchant Account Fees

Businesses often pay monthly or annual fees to maintain merchant accounts and potential fees for chargebacks, refunds, or PCI compliance. Subscription-based businesses might face higher recurring merchant fees due to frequent billing cycles and increased risk management needs.

They consolidate services, including onboarding, account management, compliance management, and dispute handling. Providers also offer customer support, reporting tools, and value-added services that can reduce administrative burdens for businesses. Additionally, merchant service providers streamline the complexities of PCI compliance and regulatory adherence, relieving businesses of substantial operational burdens and legal risks

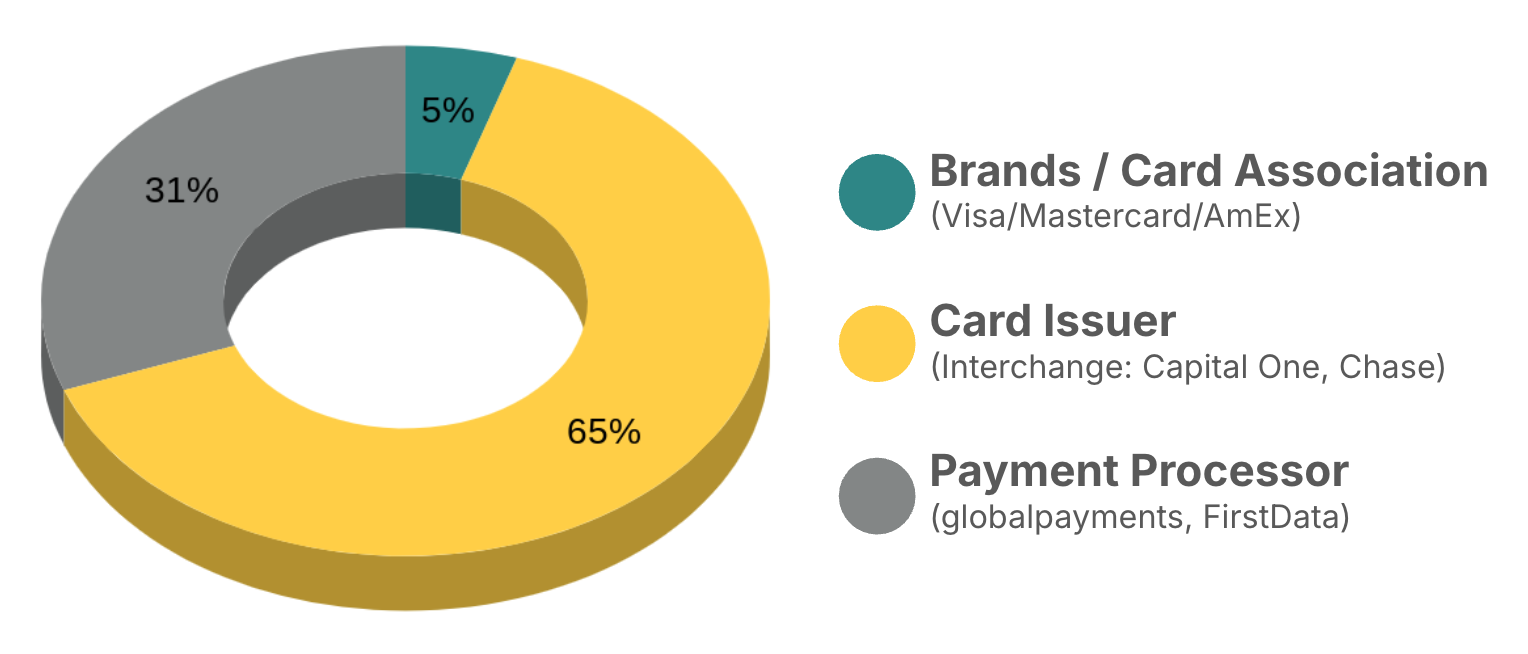

Where Do Payment Processing Fees Go

Figure 1: Chart of payment processing fees

Payment processing fees are distributed among several key players in the transaction ecosystem, each providing essential services that ensure secure, seamless, and efficient payments. These fees support the infrastructure, technology, and risk management functions delivered by card networks, payment processors, and merchant service providers.

Card Networks and Issuing Banks

They assume the largest portion of risk by managing credit and transaction authorizations, fraud prevention, and rewards programs. The fees help sustain these critical services, maintain infrastructure, ensure data security, and support customer loyalty programs. Additionally, interchange fees incentivize banks to issue and manage credit and debit cards, helping to fuel consumer spending and broader economic activity.

Hidden Costs You Might Be Missing

Most people don’t realize how costly it can be for businesses to rely on inefficient systems for processing payments.

Hidden Costs and Impact of Data Silos

Besides direct transaction fees, businesses also bear hidden operational costs, often resulting from inefficiencies and fragmented payment systems. These indirect costs include:

Manual Reconciliation Efforts

Without integrated systems, finance teams spend significant time manually reconciling transactions across multiple platforms, increasing labor costs and potential for errors. These manual processes often result in data discrepancies, leading to financial inaccuracies, increased audit risk, and potential loss of credibility.

Delayed Cash Flow

Inefficient processing and manual workflows slow invoice generation, prolong payment cycles, and negatively impact cash flow. Delays in payment processing hinder financial forecasting, disrupt business planning, and may necessitate additional working capital or costly short-term financing solutions.

Missed Revenue Opportunities

Disjointed systems can obscure valuable customer data, limiting opportunities for upselling, cross-selling efforts, and targeted marketing campaigns. This lack of integrated insights restricts businesses’ decision-making, negatively impacting customer retention, revenue growth, and competitive positioning.

Increased Security and Compliance Risks

Fragmented data management systems heighten the risk of data breaches, identity theft, and non-compliance with regulatory standards, leading to substantial fines, legal liabilities, and reputational damage.

Understanding these broader implications emphasizes the need for a comprehensive payment strategy beyond basic fee management.

The Value of Salesforce Payments Integration

Integrating payments directly into Salesforce significantly mitigates these hidden costs by streamlining payment operations within a single cohesive platform. Key benefits include:

Automated Payment Workflows

Seamlessly integrating invoicing, billing, and payment processing eliminates manual data entry, decreasing reconciliation errors and significantly shortening payment cycles. Automation also ensures consistent billing schedules, timely follow-ups, and streamlined reminders, dramatically improving cash flow management. If you’d like to learn more, explore our video on how to take payments with Chargent Payment Console.

Enhanced Data Visibility

Real-time payment insights integrated with customer data provide comprehensive visibility, empowering teams to make data-driven decisions quickly. Salesforce’s powerful analytics and reporting tools deliver actionable insights that drive strategic planning, operational efficiency, and proactive customer service strategies.

Improved Customer Experience

By providing a centralized, streamlined payment interface, Salesforce integration allows faster transaction processing, easy access to billing history, simplified dispute resolutions, and personalized service interactions. These capabilities enhance customer satisfaction, loyalty, and lifetime value.

Optimized Resource Allocation

Integration reduces the administrative burden by automating routine payment processing tasks. Employees previously occupied with manual, repetitive tasks can focus on strategic, revenue-generating activities, thereby increasing overall business efficiency and profitability.

Security and Compliance Cost Considerations

Integrating payments within Salesforce allows businesses to centralize and significantly simplify their compliance and security processes, offering several key advantages:

Unified Compliance Management

A single integrated platform simplifies PCI DSS (Payment Card Industry Data Security Standard) compliance by providing built-in tools for data encryption, secure data storage, and robust access control. Centralized data management reduces the complexity and costs associated with periodic compliance audits and risk assessments.

Enhanced Security Controls

Salesforce’s enterprise-grade security infrastructure includes advanced encryption, multi-factor authentication (MFA), robust identity and access management (IAM), and sophisticated fraud detection capabilities. These combined measures significantly mitigate the risk of unauthorized access and protect sensitive customer and payment data.

Reduced Operational Risk

Centralizing compliance and security management within Salesforce minimizes exposure to potential vulnerabilities across multiple disconnected systems. This cohesive approach substantially lowers the risk of costly data breaches, regulatory fines, legal repercussions, and brand reputation damage. For more information explore our blog post; an explanation of why you need to take payments in SalesForce.

Maximize ROI with Salesforce-Integrated Payments

Payment processing costs extend far beyond transaction fees. As we’ve highlighted in this article, data silos, manual workflows, and compliance burdens quietly erode profit margins every day. For forward-thinking businesses, the solution isn’t just a better payment processor – it’s a better integration strategy.

Integrating payment processing directly within Salesforce provides businesses with a strategic advantage by addressing these underlying issues. Salesforce integration streamlines operations, significantly reduces costs related to manual processes and reconciliation errors, enhances security and compliance management, and delivers a superior customer experience. By consolidating payment processing into Salesforce, businesses can effectively maximize their return on investment (ROI), enabling them to focus on strategic growth initiatives and long-term profitability. In an increasingly connected and competitive marketplace, investing in integrated payments within Salesforce isn’t just smart – it’s strategic.

Ready to Explore Salesforce Payments Integration?

If your business is looking to reduce costs and drive growth through smarter payment workflows, integrating payments in Salesforce might be your next big advantage. Let’s talk about how to make it happen.