Everything You Need To Know About Address Verification Service (AVS)

Payment fraud is a growing concern for online businesses, especially as card-not-present (CNP) transactions become more common. Whether you’re running an e-commerce store, subscription service, or donation platform, protecting customer data and minimizing chargebacks is mission-critical. One of the most effective fraud prevention tools available is the Address Verification Service (AVS) – a security layer that validates billing address details to detect and deter fraudulent transactions.

In this guide, we’ll explore what AVS is, how it works, why it’s essential for your business, and how Chargent’s Salesforce-native tools make implementation seamless and effective.

What is Address Verification Service (AVS)?

Address Verification Service (AVS) is a fraud prevention system used during credit card or debit transactions to verify that the billing address entered by a customer matches the address on file with the card issuer.

AVS is primarily used in card-not-present (CNP) transactions, like e-commerce checkouts or phone orders, where the physical card isn’t presented for verification. AVS compares numeric components of the billing address (typically the street number and ZIP or postal code) against the data held by the cardholder’s issuing bank.

If the information matches, the transaction can proceed. If it doesn’t, the merchant receives an AVS response code indicating a mismatch, partial match, or other outcome.

Why Your Business Needs AVS

AVS is not just a technical feature – it’s a strategic asset for businesses that want to thrive in an increasingly digital and risk-sensitive economy. Here’s a deeper look at the wide-ranging benefits AVS provides and why it should be a core part of your payment security approach.

Fraud Prevention at Scale

Every online business is vulnerable to fraudulent transactions, especially in card-not-present (CNP) environments where the customer and their physical card are not present. AVS adds a key layer of protection by comparing the submitted billing address with the one on file at the issuing bank. This real-time check can help catch fraudulent attempts before a transaction is completed.

AVS is particularly effective against:

- Stolen credit cards being used for purchases

- Bot-driven fraud attempts using synthetic identities

- Social engineering attacks involving compromised personal data

By stopping these transactions early, you reduce the downstream costs of fraud investigations, refunds, and recovery.

Reduction in Chargebacks and Disputes

Chargebacks are not only financially damaging – they’re time-consuming and can erode merchant reputation. High chargeback ratios may even lead to penalties from payment processors or a loss of processing privileges.

Using AVS to filter out risky transactions upfront significantly reduces the likelihood of customers disputing charges, especially for reasons like “unauthorized purchase” or “fraudulent transaction.”

Improved Authorization Rates & Conversion Balance

Merchants walk a fine line between preventing fraud and approving legitimate transactions. AVS allows you to make smarter authorization decisions by leveraging address data as a risk signal.

- If the AVS result is a full match, the transaction can be confidently approved.

- If it’s a partial match, you can apply internal rules or escalate the transaction for review.

- For no matches, you can trigger fraud workflows, request customer verification, or block the transaction entirely.

This nuance helps businesses avoid false declines, which can frustrate customers and impact lifetime value. With AVS, you approve more good transactions while stopping the bad ones – a critical metric for growing e-commerce and subscription models.

Granular Risk Segmentation

AVS enables transactional decision-making at scale. You can segment risk based on country, ZIP code, AVS code, and even transaction size. This is especially useful if you:

- Operate in multiple regions with different fraud profiles

- Sell high-value goods or digital products

- Have a recurring billing model where customer trust is key

For example, you might allow ZIP-only matches in low-risk countries but require full address matches in high-fraud regions. AVS lets you apply risk-based logic dynamically across your sales funnel.

Compliance & Regulatory Alignment

While AVS isn’t legally required in most cases, it is increasingly becoming a best practice standard for demonstrating due diligence in fraud prevention, especially in sectors such as:

- Fintech and financial services

- Health and wellness

- Education and certification platforms

- Nonprofits handling donor contributions

In some cases, AVS usage may help with compliance under PCI DSS, PSD2, or card network risk programs, offering supporting data that you’re proactively mitigating payment fraud.

Customer Confidence and Brand Integrity

Trust is the cornerstone of customer retention. When customers know their billing information is being verified through secure methods like AVS, they feel safer transacting with your business.

By implementing AVS and transparently sharing how you use it to protect customer data, you build long-term brand credibility. This is especially important in sectors where repeat purchases, account-based access, or subscriptions are involved.

Operational Simplicity with Scalable Automation

Modern platforms like Chargent for Salesforce make AVS implementation and configuration incredibly simple. With automated decision-making, workflow triggers, and logging, AVS becomes a low-maintenance, high-reward component of your payment infrastructure.

You can:

- Set rules for which AVS codes trigger alerts or declines

- Create custom dashboards to monitor AVS responses

- Integrate fraud data into customer support or finance teams’ processes

This means small teams can operate with the same sophistication as enterprise fraud prevention units, without the heavy IT overhead.

How AVS Works (The Process)

Understanding how AVS functions in the transaction flow is essential for configuring it effectively:

- Customer Checkout: The customer enters their billing address along with credit card details on your site.

- AVS Request Sent: Your payment gateway or processor sends the billing address to the card-issuing bank for verification.

- Address Verification: The bank checks the numeric components of the address (e.g., street number and ZIP).

- AVS Code Returned: The issuing bank sends back an AVS response code indicating the result.

- Merchant Decision: Based on the AVS code, your system can approve, decline, or flag the transaction for manual review.

It’s important to note that AVS is not a “hard block” – the issuing bank will authorize or decline the payment, and AVS simply provides additional information for the merchant to assess risk.

Understanding AVS Codes & Best Practices

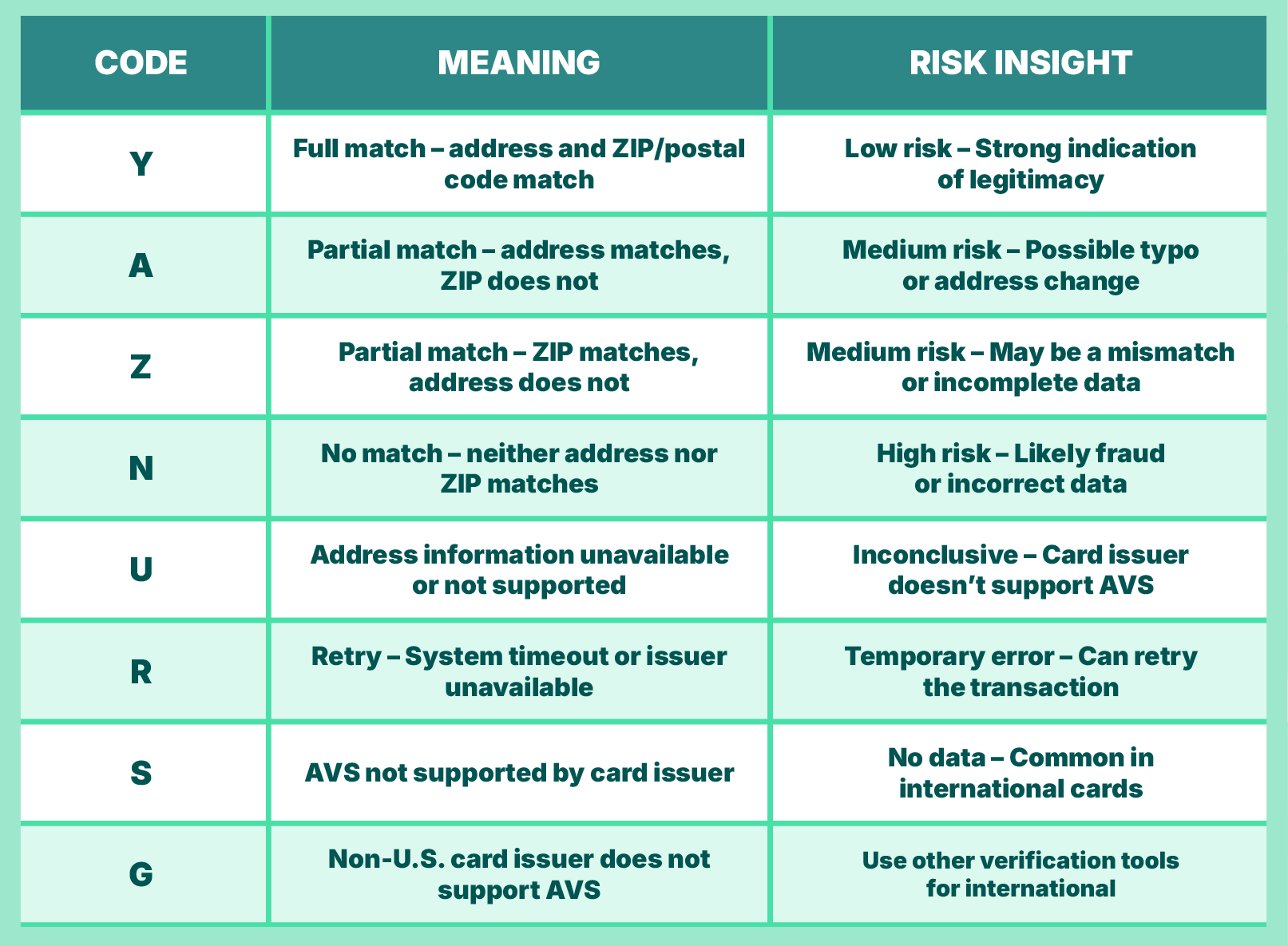

To use Address Verification Service (AVS) effectively, it’s essential to understand the response codes returned by the card-issuing bank and how to act on them. These codes indicate whether the billing address submitted by the customer matches the data on file, and they’re a cornerstone of smart payment decision-making and fraud prevention.

AVS Codes: What They Mean

AVS returns a single-letter code in the authorization response. These codes help merchants assess the level of risk associated with a transaction. Below is a breakdown of the most common AVS codes and what each one means:

Note: These codes can vary slightly depending on your payment gateway or processor. Be sure to consult their specific documentation when integrating AVS logic.

Best Practices for Using AVS Effectively

Understanding AVS codes is just the start – how you act on them determines your system’s effectiveness. Here are industry-proven best practices to help your business reduce fraud, lower chargebacks, and approve more legitimate transactions:

Combine AVS with Other Fraud Tools

AVS should be one part of a layered fraud defense strategy. For stronger results, combine it with:

- CVV verification: Ensures the customer physically has the card

- IP geolocation: Detects mismatched countries or suspicious regions

- Email/phone verification: Identifies spoofed contact info

- Velocity checks: Flags unusually high transaction volume from a single card

Chargent makes it easy to implement these tools natively in Salesforce, giving your team centralized control over fraud detection.

Adjust AVS Rules Based on Geography

AVS is most reliable in the U.S., Canada, and the U.K. Outside these regions, many issuing banks don’t support AVS or return “U”/“S”/“G” codes. For international transactions, consider:

- Accepting partial matches with additional checks

- Relying more heavily on CVV, email verification, or 3DS

- Whitelisting trusted customers based on past behavior

Avoid declining legitimate foreign transactions simply because AVS isn’t supported – it’s better to supplement AVS with other validation tools.

How Chargent Enhances AVS for Salesforce Users

If your business runs on Salesforce, Chargent by AppFrontier offers a powerful, AVS-enabled payment solution that integrates seamlessly into your CRM workflows to create a fully integrated risk management system.

Chargent supports AVS configuration directly within Salesforce, enabling merchants to:

- Automatically capture and interpret AVS codes for each transaction

- Trigger Salesforce Flows, Process Builder actions, or Apex code based on AVS outcomes

- Use real-time monitoring of AVS responses in dashboards for better fraud intelligence

- Reduce the number of false declines by tuning AVS rules over time

- Combine AVS with other fraud tools for a layered defense

By using AVS codes wisely, reviewing them regularly, and building a flexible fraud rules engine, you can turn AVS into a powerful advantage – filtering bad transactions, approving good ones faster, and protecting your bottom line.

Related Reads from Chargent:

- The Role of Compliance and Fraud Prevention in Payment Systems – Chargent by AppFrontier

- The True Cost of Payment Processing and Why Salesforce Integration Is a Smart Move – Chargent by AppFrontier

Chargent’s full-stack AVS capabilities make it an excellent choice for small to mid-size businesses looking to secure their transactions while staying native to Salesforce. Its transparency and adaptability are especially valuable for finance professionals and e-commerce leaders managing high volumes of CNP transactions.

Make AVS Part of Your Payment Security Strategy

Address Verification Service (AVS) is one of the simplest and most effective tools for defending your business against payment fraud in card-not-present scenarios.

But AVS is only as effective as its implementation. Understanding the response codes, configuring rules to match your risk appetite, and integrating AVS into a broader fraud prevention framework is key.

For Salesforce-based businesses, Chargent delivers a powerful suite of tools to leverage AVS intelligently, reduce manual effort, and protect revenue. Whether you’re building a robust payment infrastructure or refining existing workflows, Chargent offers unmatched control and visibility over your payment security.

Stay Secure. Stay Confident. Stay Chargent.

If you have questions about how AVS works or how to configure it effectively in your Salesforce environment, contact Chargent – we’re here to help.