If your business still has to accept paper checks, here are some tips to use Electronic Check Conversion (ECC) to deposit them via ACH, so you can reduce your handling of paper checks and deposit them faster.

A scientific study published in the Southern Medical Journal indicates bacteria and viruses can live on cash and checks for many days. If you have to accept paper checks, as we all sometimes do, Chargent can help you reduce your handling of paper checks and capture revenue significantly faster than traditional paper-based processes.

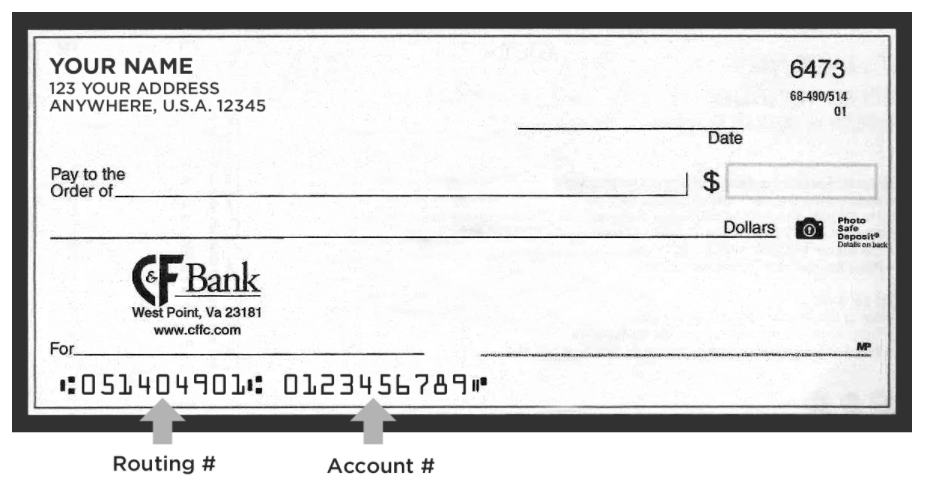

ACH, also known as Electronic Check (Cheque), eCheck, and Direct Debit, allows you to electronically process bank payments using an account number and routing number (or BSB in Australia). Entering paper checks as ECC (Electronic Check Conversion) can save time since you no longer have to physically deposit the check and it can also provide quicker insight to whether the funds are available.

As a precaution, It’s always recommended to wash your hands for the recommended 20 seconds after handling cash or paper checks. This can help minimize the spread of disease and viruses.

Accepting ACH, the eCheck processing system for the United States and Canada, does have some guidelines. NACHA (National Automated Clearing House Association) manages and administers the ACH Network while Regulation E is guided by the Federal Reserve Board and outlines the rules for electronic funds. Regulation E tells us what can be accepted electronically via ACH.

The following types of checks are allowed by NACHA, under Regulation E to be entered electronically:

- Consumer Checks

- Business Checks

- Corporate Checks

Each type of electronic transaction is reflected by an SEC Code (Standard Entry Class Code). The standard SEC Codes for ACH are POP, ARC, and BOC. This tells your processor that the check is either not physically present, the check is present and being processed while the customer is in the store, or whether the paper check is going to be processed when the customer leaves. Here is a more descriptive outline of each ACH SEC Code.

- POP (Point of Purchase): POP is used when a customer is in the store or at a booth and writes a check. The check is accepted and processed immediately as an electronic bank draft using the routing number and account number. The merchant should verify the check is signed and return it to the customer to retain for their records. The check becomes null and void.

- ARC (Accounts Receivable Conversion): ARC is used when the customer mails a check and the check is then processed electronically. The merchant must notify the customer in writing to let them know their check will be electronically entered, and the merchant retains the check for 2 years as record of payment.

- BOC (Back Office Conversion): BOC are checks that are processed in the back office after a customer leaves. The customer receives and signs a receipt acknowledging that the check will be processed electronically and the merchant retains the check for two years as proof of payment.

With some Chargent payment gateway connections, you can set the Order Source field on the Chargent Order record. The Order Source is mapped to some gateways and will send the SEC Code representing ARC or POP based on the Order Source picklist.

Check out our documentation to see if the Order Source is mapped to your gateway.

Chargent Order Source = SEC

Mail = ARC

Recurring Mail = ARC

Retail = POP

By taking these precautions and converting paper checks to electronic, you can process paper check payments more quickly, and reduce the need to travel to the bank. This will help protect your employees along with families by processing checks using the bank account payment feature in Chargent.

For full guidelines on accepting ACH you should contact your processor or merchant account. They may have unique or additional requirements such as a check reader or scanner, for depositing paper checks via ACH. Checks are required to use Metallic Ink and a check scanner has the ability for Metallic Ink Character Recognition (MICR). This can help protect you from fraud and data entry errors when processing paper checks electronically.

How to Process an ACH Bank Draft with Chargent in Salesforce:

The key is to create as few interactions with the check as possible alleviating bank deposits and prolonged handling of the paper check. Having a set process for this is highly recommended.

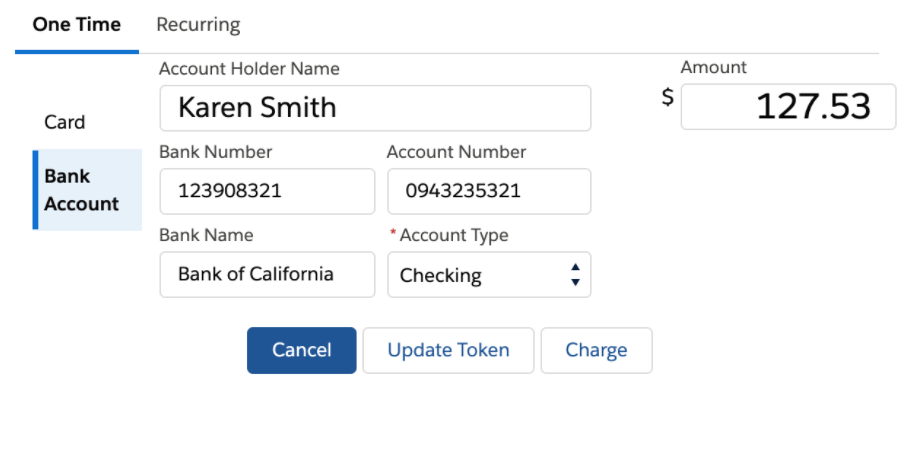

Luckily it’s pretty easy to enter paper checks into Salesforce to convert electronically using Chargent Anywhere. To enter a paper check as an electronic bank draft you need the following information from the check.

- Bank Account Number

- Routing Number (BSB in Australia)

- Amount

- Bank Account Holders Name

- Bank Name

- Check Number (optional)

To process the check using the Chargent Payment Console feature, select a Bank Account rather than Card. This will allow you to enter the above information from the check, into the Payment Console for processing.

Once you have all the information entered from the check, click the charge button. You may wish to establish additional processes like writing VOID on the paper check once the payment has been processed.

For additional precautions in handling transactions during COVID-19 check out our YouTube video How to Prevent Germs When Making Payments: