There’s no question that generating subscription revenue is the holy grail for most businesses. Membership sites and SaaS companies seem to have it all figured out. Their business models create residual monthly income, they often experience a higher lifetime customer value, and their automated systems make payments seem effortless.

Unfortunately, all that glitters is not gold. Businesses that collect recurring payments know that two simple words can disrupt the flow of everything – payment failed.

Uh oh. That’s the sound of disappointment.

Sure, your accounts receivable seemed promising on paper, but only a fraction of that amount was collected. In a panic, you scrolled through your transaction record. Then you saw it. The dreaded payment declined message.

Luckily, payment failure isn’t the end of the world. With the right AR collections process in place, your business can prevent many transactional issues and simplify the process of collecting failed payments.

What is the True Cost of Failed Transactions?

On the surface, the most evident effect of payment failures on your business is the loss of revenue from customer purchases. Research estimates that businesses lose up to 3.6 percent of their annual revenue to failed transactions. While this is a significant issue, it’s not the only thing you should worry about – the ripple effects of failed payments will usually result in:

- Customer Churn: When customers constantly experience failed transactions, they undoubtedly get frustrated and may eventually lose trust and satisfaction in your business. Low customer satisfaction may cause some customers to look for alternative services elsewhere, resulting in customer churn. If the churn rates are too high, your business costs may increase because acquiring new customers is considerably more expensive than retaining existing ones.

- Labor Costs: Failed transactions don’t stop at payment failed messages – your staff must attend to them. This can take various forms, such as answering customer inquiries, processing refunds, and troubleshooting technical issues with payment systems, and can involve several departments like finance, customer support, and IT. Handling failed payments can divert your staff’s time and effort from more productive tasks, ultimately affecting your business’s revenue.

Payment Fees: Failed payments can lead to additional costs in the form of payment fees. This is because payment processors often charge fees for each transaction attempt – successful or not. If a customer tries to complete the same transaction multiple times, these attempts will incur fees, eventually increasing your overhead costs. Additionally, if customers dispute charges because they believe the payment has failed, you may incur chargeback fees. These fees can be substantial and can negatively affect your business’s profitability.

Why Does Payment Failure Occur?

Understanding why an error message was received is vital to solving frequent failure issues. But the diagnosis isn’t always simple. Payments can fail to complete for numerous reasons, whether at the merchant, gateway, or customer level.

Some of the most common reasons that failed payments occur include:

- Insufficient Funds: Usually, payments fail simply because the customer does not have the required funds available in their account to cover the transaction – or because they have exceeded their credit limit. In either case, their bank will typically reject the payment.

- Incorrect Information: The devil is in the details, and sometimes, the answer to payment failure is there too. Errors like inaccurate card numbers, an incorrectly-entered expiration date, or a wrong billing address can cause issues during payment.

- Misconfigured Gateway: For payments to process, payment gateways must be implemented and configured correctly. Even when properly installed, incorrect settings can result in error messages and payment rejections.

- Fraud Prevention: Payment failures may also occur due to fraud prevention measures by financial institutions. However, these fraud detection algorithms can sometimes flag even legitimate transactions as suspicious and trigger payment failures. This is especially common for large transactions, international purchases, or transactions from new customers.

- Currency Mismatch: Your payment processor may also reject customer payments if they aren’t in the same currency as your payment gateway or bank account. If that isn’t the case, customers may decline payment requests if the currency conversion fees are too high.

- Network Issues: Sometimes, the issue lies not with the customer or the merchant but within the network that processes the payment. Network downtime or latency can cause transactions to fail.

If your business collects recurring payments, you will eventually deal with payment failure. But with enough preparation, you can significantly reduce these instances and recover missed payments quickly and effectively.

How to Deal With Payment Failure

Preventative measures can considerably minimize the number of failed payments you experience each month. However, it is unlikely that you will ever reach a zero percent failure rate. Even the most prepared businesses face this situation at some point. Ultimately, how you deal with failed payment recovery will determine how large of an impact churn will have on your bottom line.

It is easier and cheaper to keep an existing customer than it is to acquire a new one. With the right steps in place, you can successfully recover failed payments and ensure customer longevity.

As the top payment solution on the Salesforce AppExchange, we know a thing or two about recovering payments. Here are three proven methods for dealing with payment failures effectively.

1) Communicate the Failure

Customers may not be aware that their payment failed. While some issuing banks and systems automatically inform them of payment issues, this isn’t always true.

After the first rejected payment, send a notification to make them aware of the issue. Include a call-to-action that immediately directs them to a page where they can resolve their account.

Keep your payment failed message friendly and non-threatening, but state the next steps clearly.

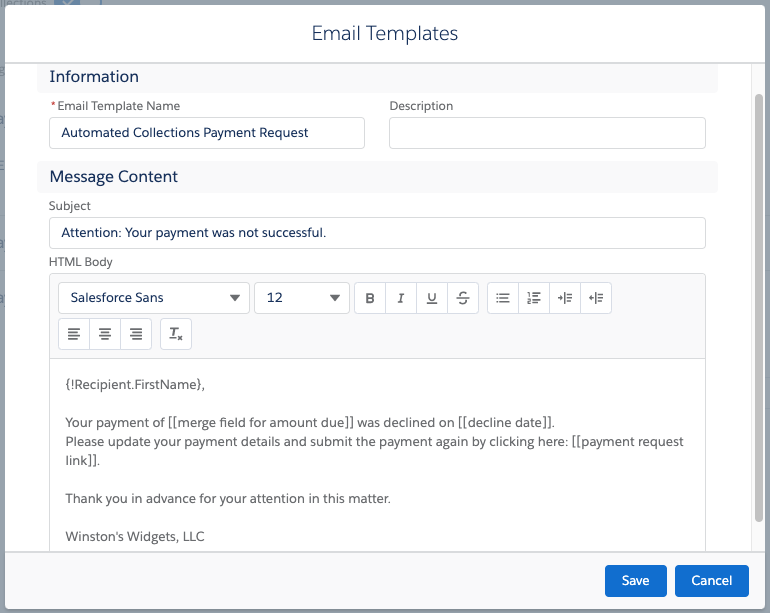

2) Establish Dunning Email Automation

Dunning is communicating with customers as you attempt to collect on accounts receivable. Usually, dunning is a significant inconvenience for everyone involved. It requires businesses to make additional effort to retrieve the payment, and it can seem intimidating to customers.

Fortunately, dunning doesn’t have to be a negative experience. With the right processes, dunning can result in positive customer experiences and lead to higher client retention.

Consider setting up an automated dunning system. After the initial notification, schedule periodic emails to remind customers that their payment is late. Offer assistance if needed and update them on what actions will occur if they don’t resolve the issue.

Chargent’s Automated Collections makes the dunning process effortless. The system allows businesses to set up effective emails that are automatically sent to past-due customers on a defined schedule. With customizable settings, Chargent users can select a specific email template and choose exactly when each email will be sent.

Deliver a positive message when reaching out to collect payment. Dunning is certainly focused on collecting revenue, but it also provides the opportunity to retain more customers, communicate with them, and build their trust.

If customers don’t complete payment by the end of the dunning cycle, reach out again for their feedback. If you can identify why they failed to pay, you may be able to offer alternative options to keep them as active clients. In addition, their suggestions may help you create a better customer experience.

3) Schedule Payment Retry Cycles

Customers may expect a direct deposit or transfer to their account on the same day their payment is processed. Sometimes, the transaction will process before their funds are available, resulting in a failed attempt.

Maximize collections by implementing automatic payment retries over a specified period (such as three retries over two weeks). This process makes collection simple for the customer – the only step required is making the funds available in their account.

Solutions like Chargent offer a major advantage – automatic retry cycles. If a payment fails, Chargent will retry the payment several times and over several days, based on your specified schedule.

Be transparent about your cycle and let customers know when to expect a repeat charge. Establishing hard deadlines will encourage them to resolve issues quickly and allow you to clear your account receivables each month.

4) Offer Customers Incentives for Prompt Payments

If you realize that most payment failures occur due to customer-related issues, you can provide hard-to-resist incentives that make them more likely to keep their payment details up-to-date.

This strategy is not only effective in reducing the rate of failed payments but also in enhancing customer satisfaction. Rewards make customers feel appreciated and valued, contributing to higher retention rates and revenue growth.

Incentives, in this case, can range from discounts on future purchases to cashback rewards and subscription extensions. Whichever incentives you choose to use, remember that clear communication is essential to ensure customers fully understand them. Additionally, personalization is critical when communicating these incentives to your customers to make the offer more relevant and compelling.

5) Have Grace Periods

Give customers ample time to submit payment before taking actions like canceling their accounts or adding late fees (if applicable). This strategy adds a human touch to how you deal with failed payments because it lets the customer know that you understand that you’re willing to work with them to find a resolution.

While grace periods can help reduce customer churn rates, they can lead to further loss of revenue if not properly managed. To ensure this doesn’t happen, you can implement several best practices.

For one, it’s important to set a reasonable duration. When deciding on the length of your grace period, try to strike a balance between providing flexibility for your customers and maintaining cash flow for your business. Therefore, the grace period shouldn’t be so long that it affects your revenue.

Secondly, ensure you communicate clearly with your customers on the grace period’s terms and conditions so there’s no confusion. It’s also best to maintain communication with the customers before, during, and after the grace period about the measures they can take to rectify the failed transactions and keep enjoying your services.

6) Offer Multiple Payment Methods

When a transaction fails, you can reduce churn rates by offering alternative ways for your customer to pay for goods or services. For instance, if the customer initiated a payment through their credit but failed, your system can automatically suggest alternative payment methods such as a digital wallet, a bank transfer, or even a buy-now-pay-later option.

This strategy can also effectively resolve failed transactions caused by mismatched currencies. By supporting local payment methods or a digital wallet that supports multiple currencies, you reduce the risk of customers failing to complete the transaction.

Maximizing Your Failed Payment Recovery Process

Payment recovery is an essential part of growing a SaaS or membership-based business. By implementing preventative measures, establishing a frictionless payment system, and adopting effective payment recovery strategies, you can turn failed payments into significant opportunities.

Want more control managing payments in Salesforce? Contact us today and find out how we can help you collect payments faster with both one-time and recurring billing.

Frequently Asked Questions

What percentage of transactions fail?

Failed transactions are a normal part of business, with figures indicating that at least 20 percent of all card transactions fail.

What are automated retry mechanisms, and how can they help with failed transactions?

Automated retry mechanisms are configurations that, as a merchant, you can set on your payment processing system to automatically attempt to process failed payments after a specified period. These configurations are especially helpful when payments fail due to network downtimes or insufficient funds in a customer’s bank account.

What should I do if a customer’s payment fails?

If a customer’s payment fails and the cause isn’t from your end, you must notify them promptly. This is because they may not be aware that the transaction didn’t go through. To do so, you can send an email or SMS or contact them another way and provide them with clear instructions on how they can resolve the issue, such as updating their payment information or contacting their bank.

How can I ensure my payment gateway is correctly configured to minimize payment failures?

Since your payment gateway can be among the reasons why your customers experience payment failed messages on their end, it’s recommended that you perform regular audits to ensure it’s correctly configured. To do this, you can test transactions occasionally or consider using multiple payment gateways to increase the likelihood of successful transactions.

How can I use automation to assist with failed payments?

Failed payments can be frustrating to follow up on, especially if done manually through customer support. With automation strategies like retry mechanisms and automated notifications, you can reduce the time and effort required.

What role does customer education play in reducing payment failures?

Though not considered by many merchants, educating your customers can help reduce the number of payment failures. To do this, you can provide helpful tips on your website or platform for customers on how to enter payment information correctly, keep card details up-to-date, and resolve common payment issues independently.

How often should I retry a failed payment?

While you can retry charging the payment again after a failed attempt, you must ensure you don’t step on your customer’s toes. This is especially true if the transaction fails due to insufficient funds or currency mismatch. The National Automated Clearinghouse Association (NACHA) generally recommends that you try up to three times to process payments after failing the first time. It’s also best practice to wait a few days before retrying the payment to give the customer time to fix the issue.