For many finance leaders, surcharging feels like a tradeoff. On one hand, card processing fees keep climbing and cut into margins. On the other, no one wants to upset customers or make the payment experience feel punitive.

But that is the wrong way to think about it.

Surcharging does not have to undermine trust. When it is introduced clearly and handled professionally, it can actually reinforce trust. It shows customers that your business is upfront, consistent, and committed to giving them payment choices.

The key is not just whether you add a surcharge. The key is how you communicate it, how you implement it, and how well you prepare your team and customers for the change.

Here are four practical strategies for rolling out surcharges in a way that protects customer relationships while helping your business recover payment costs.

1. Lead with transparency, not fine print

If you want customers to accept a surcharge, they should never feel surprised by it.

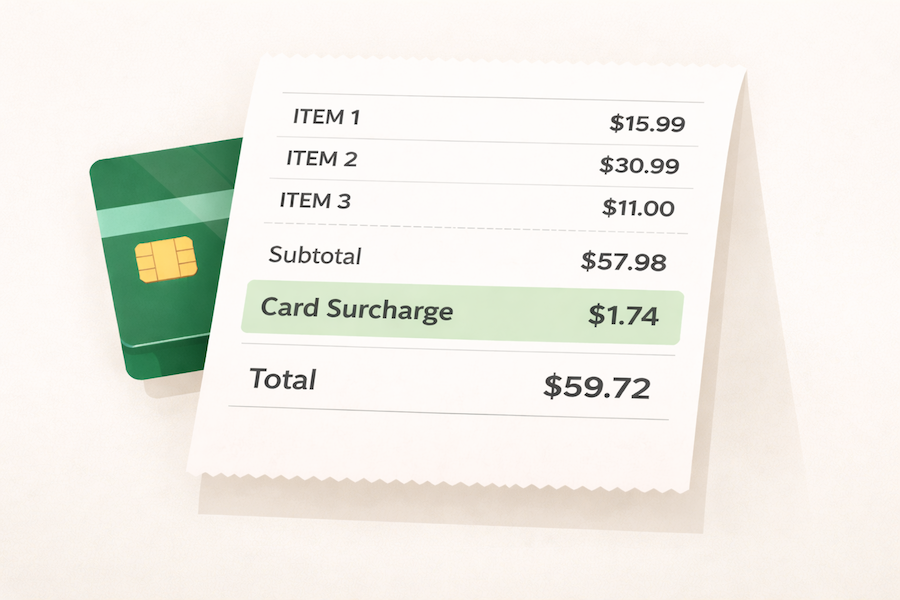

That means the surcharge cannot be buried at the last second or hidden in vague language. Customers should understand early in the payment process that a fee applies to credit card transactions and that other payment options may be available. The goal is simple: set expectations before the customer reaches the final payment step.

In practice, that means using consistent messaging across your website, checkout flow, payment pages, invoices, email reminders, and receipts. If a customer sees one message on your billing page, a different one in an email, and nothing on the receipt, trust starts to erode.

Clear wording matters too. Avoid euphemisms that muddy the issue. If you are applying a credit card surcharge, say so plainly. Do not blur it together with service fees or convenience fees. InterPayments emphasizes that surcharging is not simply a generic extra charge and that programs must follow specific rules about how fees are assessed and disclosed.

A simple message often works best:

“Due to rising credit card processing costs, a surcharge applies to credit card payments. Debit and ACH remain available at no additional cost.”

That language is easy to understand and, most importantly, sets expectations before the customer pays.

2. Explain the reason behind the surcharge in customer terms

Transparency tells customers what is happening. Context tells them why.

Many businesses make the mistake of announcing a surcharge without explaining the cost pressure behind it. Customers may then assume the company is simply adding a fee because it can. That is where resistance begins.

A better approach is to explain that card acceptance comes with real costs, and that the surcharge is designed to offset those costs rather than inflate profits. This framing matters. When customers understand that the fee is tied to processing costs, the policy feels more reasonable and less arbitrary.

This is also a good moment to remind customers what they still gain from card payments: speed, convenience, flexibility, and security. Card payments are fast, familiar, and easy to use across digital and self-service experiences. Those benefits still matter, even when a surcharge is part of the equation.

You can also reinforce that customers still have a choice. If lower-cost methods such as debit or ACH are available, say so clearly. That helps the message feel balanced. You are not forcing one expensive path. You are explaining the cost of one option while keeping others open.

The overall message should feel factual, not defensive. You are acknowledging a real business cost, explaining it honestly, and giving customers room to choose the method that works best for them.

3. Roll out surcharging with a clear operational plan

Even well-written customer messaging can fail if the rollout itself is sloppy.

Surcharging should be treated as an operational change, not just a pricing update. That means having a plan for where the surcharge will appear, which payment methods it applies to, how your staff will talk about it, and how you will monitor customer reactions after launch.

A pilot can be a smart first step. Start with one business unit, one payment channel, or one customer segment. Watch what happens. Are customers confused? Are support questions increasing? Are more customers choosing ACH or debit once the surcharge is disclosed? Those early signals can help you refine the rollout before expanding it.

It is also important to keep surcharges reasonable and aligned with whatever rules and standards apply to your business. This is not something that should feel improvised. The more structured your rollout is, the more professional and trustworthy it will appear to customers.

Technology matters here too. Manual surcharge processes create risk because they depend on people remembering the rules, calculating fees correctly, and communicating the charge consistently. A system that automates the surcharge calculation and presentation can make the process much smoother for both staff and customers.

Internally, Chargent offers surcharging as a set-it-and-forget-it capability that automates fee calculation and customer communication through our InterPayments partnership.

4. Protect the relationship by giving customers options

A surcharge lands very differently when customers feel like they still have control.

If the only message is “pay more,” frustration is natural. But when the message becomes “here are your payment options,” the conversation changes. Customers may still choose to pay by credit card, but they understand that they are making that choice with full visibility.

That is why surcharge-free alternatives should be part of your communication from day one. If you offer debit, ACH, or other lower-cost methods, make those options visible and easy to use. Do not hide them several steps later. Put them in front of customers early so they can make an informed decision.

Your team should be prepared with a short, confident explanation they can repeat consistently. Something simple works best:

“We accept credit cards, debit, and ACH. A surcharge applies only to credit card payments, so many customers choose debit or ACH to avoid the additional fee.”

This kind of language keeps the conversation practical rather than emotional. It also gives frontline staff a clear way to answer questions without sounding defensive or uncertain.

Just as important, listen to feedback after the rollout. If customers are confused, revise the wording. If staff keep getting the same question, improve the script. If one payment channel is generating unnecessary friction, adjust the experience. A strong surcharge rollout is not rigid. It is responsive.

The bottom line

Surcharging is not just a fee strategy. It is a communication strategy.

Businesses that roll it out poorly risk creating confusion and resentment. Businesses that roll it out well can recover costs while reinforcing trust. The difference comes down to transparency, explanation, operational discipline, and customer choice.

When customers know what to expect, understand why the surcharge exists, and can easily choose other payment methods, the policy feels fairer and more professional. That is exactly how surcharging should work.

And with the right systems in place, it becomes much easier to apply surcharges consistently, communicate clearly, and protect the customer experience at every stage of the payment process.

Contact us today to recover revenue with our set-and-forget surcharging feature.